Real Estate Fund Structure: The Architect’s Blueprint for Institutional Scale

The deal-by-deal syndication model is the fastest way to burn out while building a business that owns you instead of you owning it. If you’re spending 70% of your time chasing individual capital commitments for every acquisition, you aren’t an investor; you’re a professional fundraiser. You already know that the lack of discretionary capital is the primary bottleneck preventing you from executing on 8-figure opportunities with speed and precision. This friction is exactly why elite operators are moving toward a sophisticated real estate fund structure that prioritizes speed and scalability over the constant friction of the capital treadmill.

Mastering this architecture is the difference between surviving on the next acquisition fee and building an institutional-grade legacy. You’ll learn how to transition from an active operator to a sophisticated fund manager by securing discretionary capital that allows for 10-day closings. We will break down the specific legal and tax frameworks required to manage complexity at scale, ensuring your operation remains lean while your assets under management multiply. This is your blueprint for moving from the frantic energy of the solo operator into the calm, calculated execution of the boardroom.

Key Takeaways

- Break through the "syndication ceiling" by replacing exhausting deal-by-deal capital raises with a discretionary model designed for nine-figure velocity.

- Learn to architect a sophisticated real estate fund structure that separates business operations from investment assets, providing the liability protection required for institutional scale.

- Discover why a hyper-focused investment thesis serves as your "unfair advantage" when attracting the sophisticated capital of family offices and elite investors.

- Transition from a high-stakes operator to a legacy builder by leveraging collective intelligence and elite frameworks to scale without the typical operational friction.

Beyond the Syndication Trap: Why Fund Architecture is the Key to 9-Figure Growth

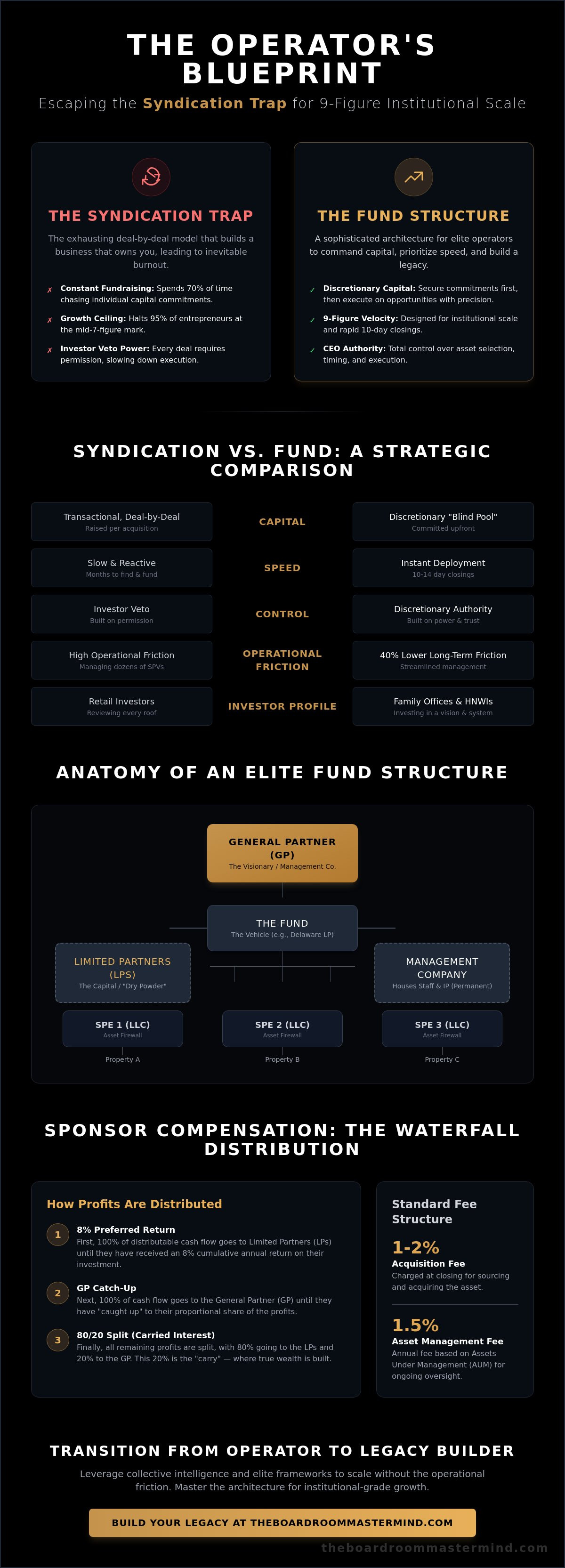

The "Syndication Trap" is a glass ceiling that halts 95% of real estate entrepreneurs at the mid-7-figure mark. You spend months hunting a deal, then pivot frantically to raise capital from retail investors. This cycle repeats until your executive team hits a burnout wall. Scaling to 9-figure assets under management requires a shift from transactional capital to discretionary capital. A sophisticated real estate fund structure allows you to secure the commitment before the acquisition. It transforms you from a deal-chasing hustler into a strategic architect who commands the boardroom.

Institutional players like family offices and high-net-worth individuals don't want to review every individual roof. They want to invest in a vision and a proven system. By moving into Private equity real estate, you signal that your firm operates with the maturity of a professional asset manager. This credibility is the difference between a $5 million joint venture and a $100 million capital commitment. It's about moving from a "hustle" mindset to building a legacy that survives market cycles.

Syndication vs. Fund Structure: A Strategic Comparison

Syndications are built on permission; funds are built on power. In a syndication, your investors hold a functional veto over every move. In a "blind pool" fund, you maintain ultimate execution power. This speed allows you to close on distressed assets in 14 days while competitors are still drafting their pitch decks. The transition to real estate private equity is the definitive move for those who value time over the frantic energy of the hunt. A robust real estate fund structure ensures your growth is dictated by your strategy, not investor sentiment.

- Control: Funds provide the CEO with total discretionary authority over asset selection and timing.

- Speed: Capital is deployed instantly when the market presents an "unfair advantage" or a motivated seller.

- Complexity: Funds require higher upfront legal compliance but offer 40% lower long-term operational friction than managing 50 separate SPVs.

The Anatomy of a Private Equity Real Estate Fund Structure

The real estate fund structure is the skeletal system of your investment empire. It dictates how you move, how you scale, and how you protect what you've built. You operate as the General Partner (GP), the visionary who identifies alpha and executes the strategy. Your investors are Limited Partners (LPs), providing the necessary dry powder while enjoying limited liability. This isn't a partnership of equals; it's a hierarchy designed for decisive action.

Successful sponsors separate their Management Company from the Fund. The Management Company is your permanent brand, housing your staff and intellectual property. The Fund is a temporary vehicle, often a Delaware Limited Partnership, that holds the assets. This separation ensures that a single property-level disaster won't jeopardize your entire enterprise. You manage the fund through a sophisticated capital stack, typically balancing 65% senior debt with 10% mezzanine financing and 25% equity to maximize your internal rate of return (IRR).

Waterfall distributions align your interests with your LPs. You don't get rich on fees; you get rich on the carry. Most institutional-grade funds utilize an 8% preferred return hurdle. Once that hurdle is cleared, a "catch-up" clause allows you to collect your 20% share of profits. Scaling these complex systems requires access to an exclusive peer network that has already navigated these institutional waters.

The Role of the Special Purpose Entity (SPE)

Every asset must be held in a dedicated SPE, usually a single-purpose LLC. This creates a firewall around each property. If a tenant at Property A files a major lawsuit, Property B remains untouched. The fund acts as the parent entity, consolidating these SPEs for streamlined reporting and tax efficiency via K-1 distributions. It's about ring-fencing risk while aggregating power.

Sponsor Compensation: Fees and Carried Interest

Institutional investors expect a standard fee structure or a variation thereof. You'll often charge a 1% to 2% acquisition fee at closing and a 1.5% annual Asset Under Management (AUM) fee to cover operational overhead. The real wealth is in the carried interest. This performance fee rewards your ability to exceed the 8% hurdle rate, transforming you from a mere operator into a true wealth architect who profits from the value you create.

How to Structure Your Real Estate Fund for Maximum Velocity

Speed is the byproduct of clarity. To reach institutional scale, your real estate fund structure must eliminate every ounce of operational ambiguity. You don't just build a fund; you engineer a vehicle for rapid capital deployment. This begins with a hyper-specific investment thesis. Generalists struggle to raise capital in a crowded market. If you target 1980s-built B-class multifamily assets in the Sunbelt with a 15% value-add target, you provide a clear product for high-level investors. Specificity is the unfair advantage that attracts $10 million checks.

Selecting your legal jurisdiction is the next move. Delaware remains the gold standard for over 65% of all Fortune 500 companies because of its sophisticated legal framework and established Chancery Court. You'll likely choose a Limited Partnership (LP) to provide clear separation between the General Partner and the Limited Partners. Once the entity is set, your Private Placement Memorandum (PPM) becomes the definitive manual for your strategy. It must be rigorous. It must mitigate risk. Most importantly, it must communicate a narrative of inevitability to your investors. Use technology to automate the subscription process. Friction in the onboarding phase kills 40% of potential commitments before the wire ever hits.

SEC Compliance: Reg D 506(b) vs. 506(c)

Choosing between these two paths dictates your growth trajectory. Reg D 506(b) relies on pre-existing relationships and forbids advertising. In contrast, 506(c) allows for general solicitation, meaning you can market your fund publicly. This is why 506(c) is the preferred choice for CEOs scaling through exclusive mastermind groups and elite networks. It allows you to leverage your public authority to fill the capital stack faster while ensuring all investors are verified as accredited.

Building Your Fund Launch Team

You cannot scale a fund from the operator's seat. You need a specialized team to handle the complexity of a real estate fund structure. This includes:

- SEC Counsel: To navigate the nuances of Reg D compliance and state blue sky laws.

- Fund Accountant: To manage complex tax distributions and K-1 reporting.

- A-Player Leadership Team: To execute the acquisition strategy and manage asset performance.

Hire a third-party fund administrator to provide the transparency that sophisticated family offices demand. This signals that you've moved beyond the hustle and into true wealth architecture. It provides an independent layer of verification that builds institutional trust.

Stop playing small and start engineering your exit. Join the Boardroom Mastermind experience to align with the world's highest achievers.

From Fund Manager to Legacy Builder: Scaling Your Capital Architecture

Transitioning from a successful operator to a legacy builder requires a fundamental shift in how you view your real estate fund structure. It isn't just about the assets under management; it's about the durability of the management company itself. To reach institutional scale, you must leverage the "Power of Proximity." Your fund's growth ceiling is often determined by the caliber of your elite peer network. Access to high-level intelligence allows you to bypass the trial-and-error phase that stalls 85% of mid-market firms.

Attracting institutional capital, specifically through family office real estate investing, demands a level of transparency and sophistication that entry-level setups lack. These investors aren't just looking for yield; they're looking for institutional-grade reporting and governance. Optimizing the real estate fund structure for institutional scale requires a robust Business Operating System to handle complex distributions without operational burnout. Systems ensure your reporting is accurate and timely, which builds the trust necessary to secure 8-figure and 9-figure commitments.

Finally, consider your exit strategy. Are you building a job or an enterprise? By structuring your management company for a future sale or as a perpetual legacy vehicle, you create value beyond the underlying real estate. Sophisticated fund managers treat their management entity as a product, optimizing it for a high-multiple acquisition by larger private equity firms or consolidating peers to dominate a specific asset class.

Auditing Your Model for 9-Figure Potential

The "Boardroom Audit" is a critical exercise for established managers who have hit a plateau. This quarterly peer review process forces you to justify your capital stack and operational overhead to those who have already achieved 10x your current volume. It's the difference between guessing and executing with certainty. Elite proximity creates an unfair advantage by providing real-time data on capital raising trends and deal flow, allowing you to pivot before your competitors even recognize the shift in the market.

Architecting Your Nine-Figure Legacy

Successful scaling isn't about working harder on the next individual deal. It's about the sophisticated architecture of your capital. You've now seen how a strategic real estate fund structure transforms a fragmented portfolio into an institutional-grade powerhouse. Moving beyond the limitations of deal-by-deal syndication allows you to unlock the velocity required for 9-figure growth. This transition from active operator to strategic owner remains the only predictable path to building a lasting legacy. You need a framework that compounds wealth without requiring your constant intervention at the ground level.

The Boardroom Mastermind provides the exact blueprint for this evolution. We facilitate quarterly in-person business audits with 8 and 9-figure CEOs who've already navigated these high-stakes complexities. You gain immediate access to the REWW legacy of institutional-grade scaling and an exclusive peer-to-peer network for capital and deal flow. Stop guessing at your growth strategy; it's time to step into the inner circle where elite execution is the baseline requirement. Join the Inner Circle: Apply for The Boardroom Mastermind Membership. Your ascent to the top is a logical conclusion when you have the right access and the right peers.

Frequently Asked Questions

What is the most common legal structure for a real estate fund?

The Delaware Limited Partnership (LP) is the dominant legal framework for scaling a real estate fund structure in the United States. You'll typically establish a General Partner (GP) entity to manage operations and a separate Limited Partnership where investors contribute capital. This architecture provides robust liability protection and tax efficiency through pass-through treatment. It's the standard choice for 90% of institutional-grade private equity vehicles.

How much capital do I need to start a real estate private equity fund?

You should prepare to commit 1% to 5% of the total fund size as a sponsor co-investment. Institutional LPs demand this alignment to ensure you've got significant skin in the game. If you're launching a $100 million fund, expect to bring $1 million to $5 million of your own capital to the closing table. This personal stake transforms you from a mere operator into a true partner.

Can I structure a fund if I only have a few deals under my belt?

You can launch a fund with as few as 3 to 5 successful exits by utilizing a Deal-by-Deal or Pledge Fund model. These structures allow you to build institutional credibility without the immediate pressure of a blind pool. Sophisticated investors care about the precision of your strategy and your ability to replicate 18% plus returns. Focus on the data from your previous 24 months of operations to prove your thesis is scalable.

What is the difference between an open-ended and closed-ended fund?

Closed-ended funds operate on a fixed timeline of 7 to 10 years, while open-ended funds provide perpetual life and periodic liquidity. A closed-ended real estate fund structure is ideal for value-add strategies where you need a 3 to 5 year window to execute a turnaround. Open-ended funds allow investors to redeem shares at specific intervals, usually after an initial 2 year lock-up period, making them better for stable, income-producing assets.

How do real estate fund managers get paid?

Fund managers typically command a 2% annual management fee and a 20% performance promote after hitting an 8% preferred return. This 2 and 20 logic remains the industry benchmark for high-performance teams. Some elite managers now use tiered promotes that scale to 30% or 40% once the fund surpasses a 15% or 20% internal rate of return. This structure ensures your wealth compounds alongside your investors' success.